The benefits of a mid-life crisis

What do you want to be when you grow up? It’s a question you often get asked at the age of five but not very often at the age of 50.

It’s a question that doesn’t get asked because generally we think people in the middle of their lives don’t need much support.

crisis

NOUN plural crises

- A time of intense difficulty or danger.

- A time when a difficult or important decision must be made.

What do you want to be when you grow up?

We often hear about the support needed for younger and older age groups but not much about the group in the middle. As the Resolution Foundation has highlighted, the labour market has, on the whole, not been kind to millennials in terms of pay, progression and security at work, the housing market and ability to save. For older ages we’ve also seen the beginning of an increase in pensioner poverty after several decades of welcome decline (JRF, 2017).

On many measures those in mid-life are doing OK: home ownership and employment rates are high and salaries are among the highest they will be. At this age, the gap between what you pay in tax and the services and benefits you get from the state is at its widest. From a public policy perspective, you’re doing all right.

But are you?

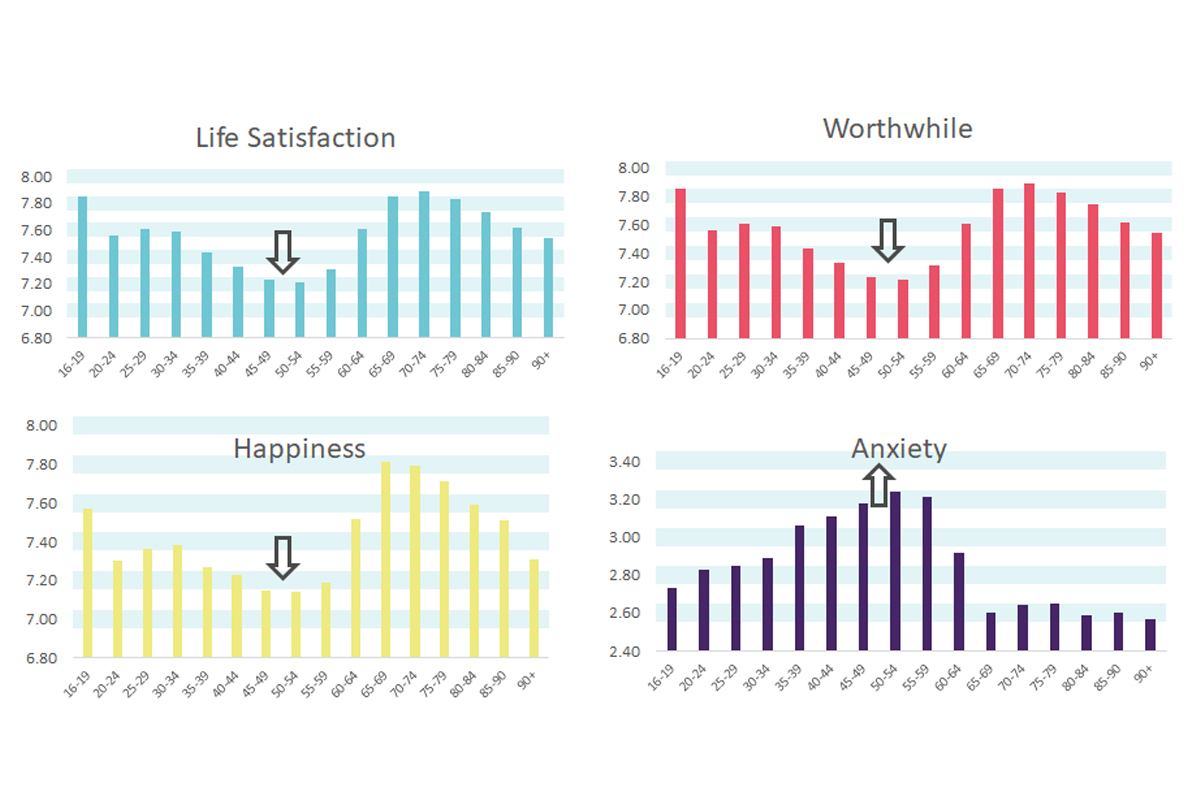

This is a time of life when your own personal wellbeing in terms of life satisfaction, happiness and feelings of life being worthwhile are at their lowest, whereas feelings of anxiety are at their peak.

Average personal wellbeing measures by age

Source: Annual Population Survey, Office for National Statistics Average Personal Well-being Ratings: by age, 2012-2015

Average personal wellbeing measures by age

Source: Annual Population Survey, Office for National Statistics Average Personal Well-being Ratings: by age, 2012-2015

This is also the period when you are most likely to be providing unpaid care for someone else. If you’re in the ‘squeezed middle age’, you may have caring responsibilities for both older and younger generations. Although you may have higher than average earnings, you also have higher than average expenditure.

While salaries are higher than they are at other ages, they tend to have peaked and then decline until you leave work. Speaking of which, it is also the start of a steady decline in employment rates: more than eight out of ten people are working in their early 50s compared to just over half of people in their early 60s.

We know that many people are not saving enough, with an estimated 12 million people heading towards an insufficient retirement income. Mid-life is also the start of a steady increase in the prevalence of long-term health conditions.

With a rising state pension age and people living longer than ever before, there is a greater need to plan and prepare for your future life than ever before. While many are thriving and enjoying their work, many others are not. For some, it might be disheartening to hear that at the age of 50, you probably have another 888 Monday mornings until you are eligible for your state pension. This may feel like a daunting prospect. It’s probably a good idea to plan what you want to do with that time, but the availability of careers advice or training opportunities is limited.

No wonder we have stereotypes and jokes around this being a period of mid-life crisis.

With many more of us facing the prospect of living until 100, 50 will increasingly become the halfway point.

A mid-life crisis

A ‘crisis’ might not be a bad analogy. The origins of the word also mean ‘a time when a difficult or important decision must be made’, which is perhaps a fitting and useful way of thinking about how we take stock and think positively about the rest of our longer lives.

With many more of us living until 100, 50 will increasingly become the halfway point: an important time to take stock, reflect and plan for the decades ahead. As a society, it’s important to think about how we will fund our future years, when and how we will work and retire, how we will spend our time, how will we maintain our health and social relationships and how we will care for those around us.

Unfortunately, the evidence also shows that, generally speaking, people aren’t particularly planning at this stage in their life. In fact most people haven’t even thought about thinking about it. As much as 57% of people haven’t thought about their hopes or ambitions for life after 60 much or at all. Most usually say it’s because they don’t tend to plan their life out in advance or that it seems too far off. It’s not for a lack of information. Perhaps this is of little wonder when current pressures in the here and now trump thinking about the uncertainty the future might bring.

People are uncertain about their future retirement income from the state and there isn’t always great trust in private pension providers. Four out of ten people who aren’t retired think that there won’t be a state pension by the time they do retire. Of 22 financial products reviewed by the FCA, pet insurance ranked among the highest in terms of satisfaction and trust. In comparison, private workplace pension products ranked 21st in terms of satisfaction and 22nd in terms of trust. People need better access to information and guidance for the most important products to their future financial wellbeing. Why plan for a future if you suspect the rules are going to change and you don’t trust the providers of your most important financial products?

These are different times, with new challenges. One thing for certain is that whoever you are, your later life will be very different from those of your parents and grandparents.

John Cridland’s independent review of the state pension age published last year was called ‘Smoothing the Transition’. Transition, because he recommended an increase to state pension age of 68 starting in 2037, but that it would be in need of smoothing for many people to mitigate the social, economic and health inequalities that could result. One of those mitigations was to introduce a ‘Mid-life MOT’ as a trigger point to encourage people to take stock and make realistic choices about work, health and retirement.

The Centre for Ageing Better has been exploring options and models with government, employers and service providers and we will reflect later on what the evidence shows us about the viability of this concept. In the meantime, it’s important that as a society we begin to plan ahead in our middle years as much as our early years. With big decisions to make in the middle of our lives, we shouldn’t let a good crisis go to waste.